Should I Buy My Dog Or Cat Health Insurance?

Ron Hines DVM PhD

When your grandparents were young, dogs and cats were property. You and I could love them, we could spoil them, and we could talk to them. We all did. But law and society granted our pets no special status, no inalienable rights, no rules regarding their welfare.

That was also a time when veterinarians like myself could not offer your dog and cat highly sophisticated (and very expensive) treatments when it became ill. In the last 50 years all of that has changed. For many of us pet owners, dogs, cats and creatures as small as a mouse have become family members. Any medical procedure available to you, should you become ill, is now available for your pet.

Our pets were always very dependent on us. But over the last 50 years, many things have made us more dependent on them. The first is emptiness and loneliness: Family size is smaller. Relatives live farther apart. Two-working partners leave little time for relaxing and togetherness. Our kids grow up and move away. If we are lucky, they call us once in a while. The interpersonal support systems of small-town America are fading away. Religion plays a smaller role in the lives of many of us.

The second is the ever-growing influence of pernicious technology in our daily lives. The negative effects of the Internet and social media isn’t just about teens and sub-teens. (read here) Media has become more strident in emphasizing consumerism, immediate gratification, superficiality and sensationalism. That makes people more likely to long for a non-judgmental furry friend. One with no ulterior or financial motives. One that doesn’t hold grudges. (read here)

Your pet is happy and content with a simple pat on the head. It senses when you are happy, it senses when you are sad or stressed. Regardless of its health, it is happy and content when you are happy and content. That is why many people now regard their pets as essential, supportive “non-human-being” family members. An integral parts of their life experience rather than a possession. It occurs to many of us: If the rest of our family has health insurance, why should my pet be left out?

The Companies Selling These Policies

Many traditional American casualty insurance companies, and some newcomers, now see pet health insurance as profitable. If you arrived at this article through a Google search, those companies probably took up the top three quarters of your search results. All describe their policies in glowing terms. But the most accurate pet health insurance data is probably that which is generated by the Agria Pet Insurance Company you see in the photo above. Agria operates in the UK and Western Europe. Agria has been in the business of offering livestock risk insurance since 1890. So, their business model is likely to be the most realistic in offering pet owners policies that their purchasers like but that still yield the Company sufficient profit to stay in business. In 2021, Trupanion, realized that and recruited the CEO of Agria’s UK branch in an attempt to emulate the European model. The “sweet spot” in benefits and premiums that please most pet owners and the company is very narrow. They know that being too generous in their benefits guarantees that they will not be in business for long. They also know that being too stingy in the benefits that they provide will produce negative online reviews that will put them out of business almost as fast.

Pet owners in Europe and the UK have been considerably more likely to purchase these “third-party” pet health polices than in the United States. One of the reasons might be that in the United States, veterinarians are not currently allowed to sell individual insurance plans. Only licensed insurance agents can do that. An exception are “wellness plans” sold through corporate practices such as VCA/Mars. At some point in the future those two corporate groups, insurance companies on one side and the huge, multi-site corporate practices allied with lucrative veterinary school-based specialists on the other will most likely clash. So whether you plan to seek your pet’s veterinary services at an independent veterinarian-owned animal hospital or through one of the nationwide locations of corporations like VCA should factor into your decision.

The second reason pet insurance has been slow to catch on in the USA is probably because each of the 50 states has its own complex insurance rules and regulations.

Which People Are Most Likely To Purchase Dog And Cat Health Insurance Policies?

Today many more American dog owners than cat owners purchase pet health insurance policies. It remains unclear as to why that is. Many who purchase these policies for their pets are millennials, new to the responsibility of pet ownership.

The AVMA commissioned Mississippi State University to conduct an email survey of dog owners regarding the characteristics of the purchasers of dog health insurance policies. I have issues regarding their findings, but of the 645 people who responded, 67.6% had purchased dog health insurance policies. That is not an expected result because that same year the pet insurance industry claimed that only 2.3% of the dogs and 0.4% of the cats in America were insured. The AVMA, like any union, is focused primarily on increasing their member’s incomes, not necessarily on the best interests of the general public. Regardless of their motives and accuracy, their study found that if your dog sleeps in bed with you (66.4% did), you were twice as likely to buy your dog health insurance than if it didn’t (33.6%). Of dog owners who bought insurance, 23% of the pets slept on their bedroom floor, 22% sleeps in a crate, 3% slept somewhere else in the house and 3% slept in the backyard. 63.5% of the policies were bought by women. Two thirds of those with policies had an income of $55,000 or more (in 2019). Almost half of the dogs were purebred. Less than half were spayed or neutered. Most were smaller breeds of dogs. (read here)

By state, in a 2021 survey, California led in the Nation in insured dogs at 19.3% in 2021. New York was next at 8.4%. Virginia was the lowest at 3.2%. Lower income states were not included. In Canada, Ontario led at 38.9% with the lowest being Nova Scotia at 4.3%.

In another 2019 survey conducted at the VCA/Blue Pearl veterinary specialist’s hospital in Irvine, California, 28.5% of pet owners presented pets that had insurance policies. Forty percent had selected the company providing the insurance through their online research. Seventy-seven percent were satisfied with their pet insurance plan and 73% would recommend that plan to a friend. The owners of pet insurance polices were considerably more likely to approve expensive tests when suggested. The majority of pet owners who purchased pet insurance had college degrees. Being a highly affluent population, and a hospital devoted to expensive procedures, those numbers probably do not reflect nationwide trends. (read here)

If I Purchase A Dog Or Cat Health Insurance Policy, Will I Save Money?

Probably not.

The pet insurance industry has set their rates to ensure that the great majority of pet owners will not save money on veterinary bills over the life of their pet. That is the only way they can remain in business. What they actually do offer you is a way to ensure that when a serious policy-covered health issue arises, the bill will be paid (minus co-pays if any). So, these policies are a good way to insulate your financial obligations from peaks and valleys by converting them into more modest monthly amounts. (read here) Unexpected and expensive events do occasionally occur. (read here) The only other way I know of to insulate yourself from the pain of an unexpectedly high veterinary bill is to set aside money each month especially earmarked for your pet(s) health needs. But how many of us have the willpower to do that?

Don’t compare these policies to Medicare or Medicaid. Those programs are highly subsidized by the government. Your Medicare premiums only account for ~15% of what doctors and hospitals eventually are paid. Pet insurance is more like home insurance or car insurance. In home insurance, about one person in 20 make a small to moderate claim per year and one in 60 makes a major claim. Even less (~3%) of people with comprehensive auto insurance may a claim in any given year. So, many pet insurances companies sweeten the pot a bit with the inducement of a free “wellness” checkup each year. If the “wellness” checkup includes a complete blood panel and urinalysis, it might catch health issues before they become a more serious problem. That is in both your pet’s and the Company’s favor.

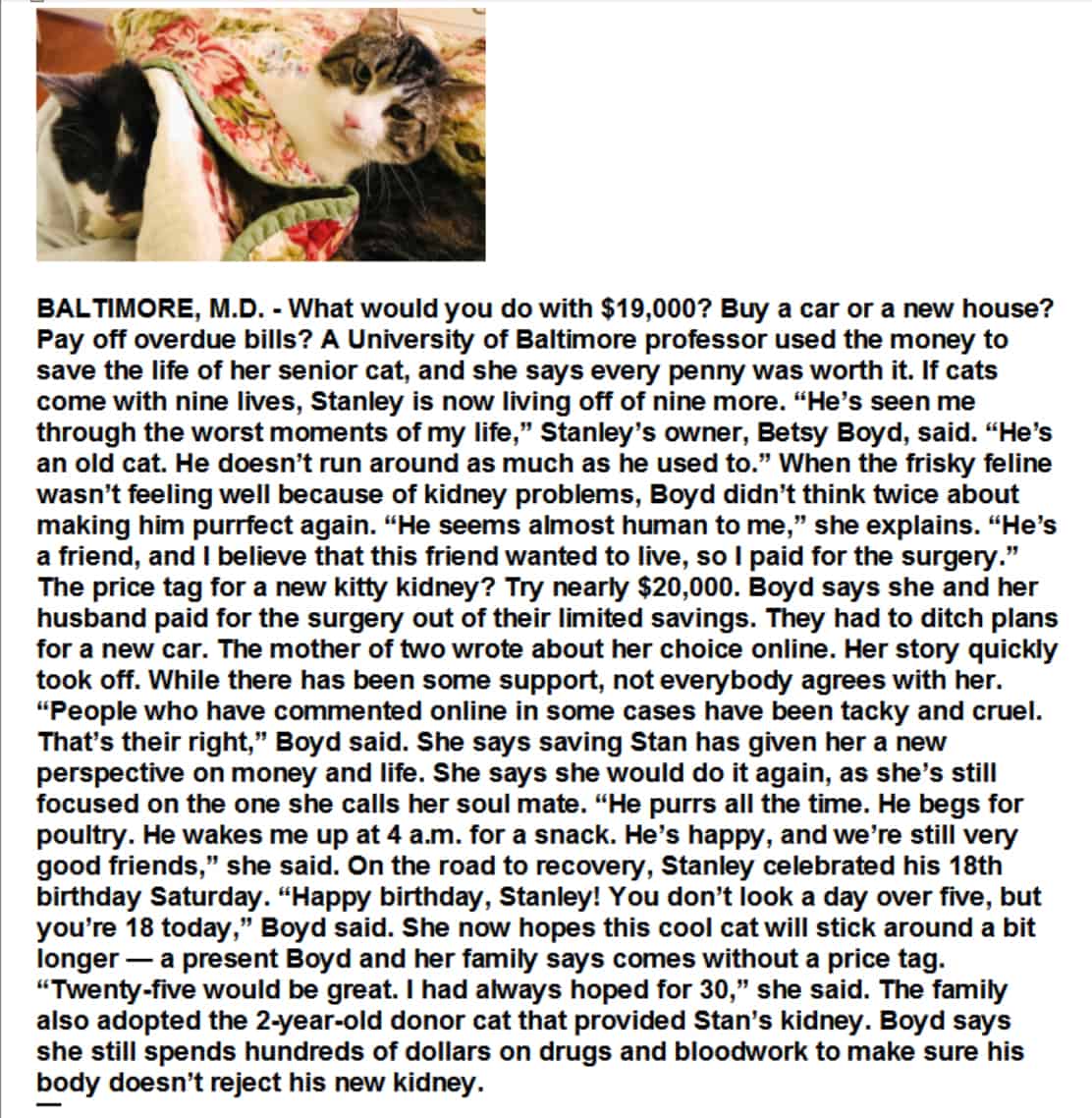

It’s just good business for pet insurance companies to promote and advertise the 1 in ~50 pet owners who benefited financially: The pet owner whose dog needed a $12,000 portosystemic shunt ligation soon after the owner bought a policy. Some companies would have denied that claim because 90%+ of pets with PSS are born with that problem (=congenital). Or the cat that needs an $19,000 kidney transplant. Or the Cavalier King Charles Spaniel that needs Dr. Uechi’s $30,000 heart valve replacement.

Then Who Should Purchase A Pet Health Insurance Policy?

The ability to pay for major veterinary services if and when the need arises is a major challenge for many pet owners – sometimes so great that owners opt for euthanasia. Pet health insurance is a tool that can often prevent that. As I mentioned, the only other option is for you to open a separate savings account for your pet. One dedicated to paying your pet’s medical expenses when the need arises. Few of us have the temperament or dedication to do that. And with that second approach, there will always be those one in 20 or one in 60 pets who experience medical costs greater than what you have accumulated at that date. Purchasing a policy gives you immediate peace of mind regarding that. However, be sure to carefully read the fine print as to which and when health problems become reimbursable.

It has been found that dog owners who have purchased insurance policies for their pets spend more at their veterinary visits than those that do not have insurance. That is the AVMA’s hope. Naturally, the premiums quoted to you will depend greatly on your pet’s age when you first apply. These companies know that big bills are much more likely to occur late in your dog or cat’s life. Policy cost will also differ by breed. These companies know that certain breeds of dogs and cats have longer life spans and fewer health issues than others.

Are There Other Benefits When I Purchase A Pet Health Insurance Policy?

Yes,

There is another important positive for me when you purchase health insurance for your pet. It removes a major stress factor from your veterinarian’s mind. Veterinarians love to offer your pet the best care possible. But they hate to discuss its cost. Many pet owners today expect their animal’s care to take precedence over a veterinarian’s need to earn a reasonable living. They see their large bill, but quite a few pet owners do not realize how large a portion of that bill represents the salaries of front desk and nursing labor, medication costs, equipment costs, building costs, continuing education costs and the monthly loan payments most young veterinarians must make to repay their student loans. Private workplace human health insurance plans or Medicare shield people from considering those issues when they themselves become ill. So, veterinarians tend to breathe a large sigh of relief when they find out that they do not have to confront that issue when it pertains to your pet. (read here and here)

Your veterinarian’s views on pet insurance could easily change in the future. As these insurance companies expand their client base, they will be tempted to lower their costs to increase profits for their shareholders. In the human medical field, that has led to managed care in which companies rout policyholders to the lowest medical bidder. That invariably lowers the quality and timeliness of the care received. More widespread acceptance of pet health insurance could also increase the cost of veterinary care for those who do not purchase pet health insurance and drive up the monthly premium cost for those who do buy policies, as it has in the UK and Europe. see here:

If I Buy Pet Health Insurance Will My Dog Or Cat Have A Longer Life?

Perhaps.

If purchasing pet health insurance motivates you to take your cat or your dog to your veterinarians as soon as you are suspicious that something is not right, yes – your veterinarian might catch a serious health issue while it is still more treatable or curable.

Also, having assured access to highly sophisticated diagnostic tests or complex surgery that you could otherwise not afford will at times be lifesaving. However, not nearly as life extending as purchasing or adopting a breed of dog known for long longevity. If you want your pet to be with you as long as possible, select a breed and a family line within that breed known for its good health and longevity – not the trendy breed of the hour, the movie star’s choice or for its cuteness.

All pet insurance company actuaries know exactly which the shorter-lived breeds are. So, the monthly cost of your pet’s insurance policy will reflex your pet’s breed risk as well as its age. Online and in print data on how long specific dog breeds are likely to live and which health issues affect which breeds are highly inaccurate. That is because that information is generally furnished by professional breeders, the AKC or the CFA, not neutral sources. (read here)

What Should I Be Looking For In A Pet Health Insurance Plan?

I would be looking for a plan that is most liberal in covering the costs of catastrophic illnesses your pet might encounter – not routine veterinary care, “wellness exams” or vaccinations. I would stay with companies that have a longstanding, positive reputation in the insurance world. Among those companies, there should only be small difference in policy costs for similar or identical coverage. If you like your auto or home insurance company, ask them if they also offer pet health insurance. They might even offer you a discount based on your multiple policies.

An initial low monthly premium might also be bait to induce you to sign up. So read their policy carefully to see if your future monthly payments are based on increases in the cost of living, your pet’s payout experience or the company’s pet owner group experience, or if they can increase your monthly premium or cancel your policy without explanation.

More About The Fine Print

In most plans, you’ll pay your veterinarians and then file a claim. It is common for you to be required to pay 10-30% of the bill if the claim is accepted.

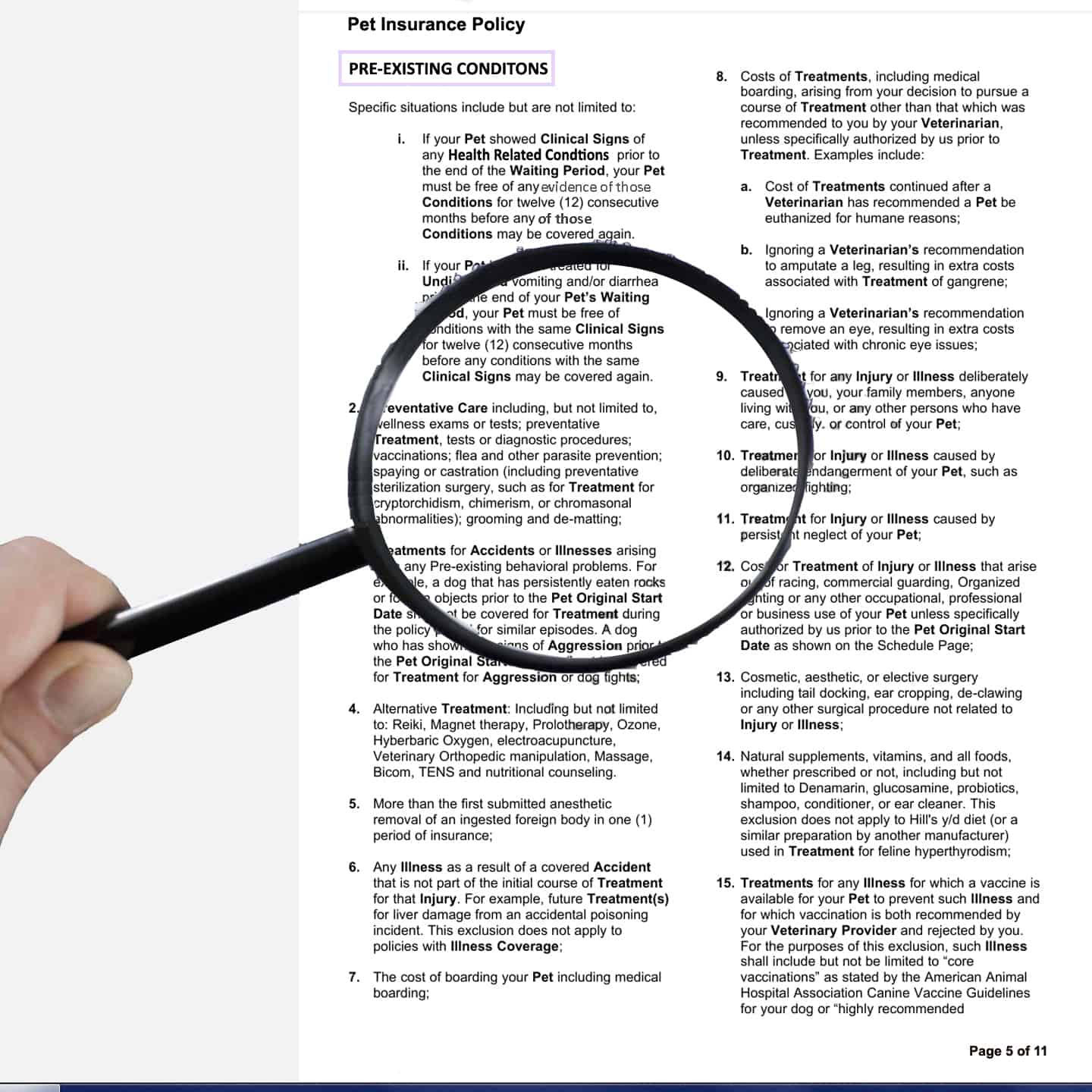

Pre-existing conditions or inklings that they might later appear are rarely covered. A great fear of these companies is that you might already be suspicious that something is amiss when you purchased your policy.

A very basic plan might cover only injuries due to accidents. Other, more expensive plans cover a variety of illnesses that were unpredictable. Some even cover burial or cremation expenses. Some plans limit dental coverage, others do not. If any tartar has been noted in your pet’s veterinary records prior to beginning coverage, some plans exclude or limit later dental coverage for your pet.

Some plans limit coverage for medical conditions that are known to be hereditary for a specific breed of dog or cat. Policies for breeds known to incur high medical bills will probably cost you more or, perhaps, be unavailable. By law, veterinarians are currently prohibited from selling pet insurance. To sell insurance, one must be a licensed insurance agent. Your vet most likely isn’t. It is wise to ask your favorite veterinarian, off the record, what his/her experience with a particular pet insurance company has been before purchasing that policy. Ask what the timeframe will be before you receive your reimbursement check. Get everything in writing. Be sure your state Board of Insurance will assist you if problems later arise. Yelp and websites like it are always a starting place to view common issues with specific companies. But remember that people with perceived bad experiences are much more likely to contribute those reviews than people with good experiences.

More About Common Exclusions

In some policies, health issues the companies deem to be the result an aggressive or abnormal pet personalities is sometimes considered cause to deny a claim. That is particularly true when injuries resulted from a dog or cat fight.

When your pet is sick, you are never at your happiest. Be patient and polite when dealing with these insurance companies. Some can even cancel a policy for what they perceive as rude interactions with their claims adjusters.

Legitimate private health insurance companies require a complete medical examination and your complete medical history before they will quote you your monthly premium. Think about it – shouldn’t that also go for your dog or your cat as well? Beware of companies that tell you that they will insure your pet without access to that same important data. Most, perhaps all, legitimate pet health insurance companies require that your pet have a complete physical examination (at your cost) within the last ~6-12-month preceding your application. Reputable companies might even have reviewing veterinarians on board or available to look over those results. Perhaps, depending on your pet’s examination results or age or breed, those veterinarians or trained agents might require additional tests to be performed before making their decision. I would be very cautious about purchasing any pet health care offering for my dog or for my cat that did not require a thorough health examination before they agree to insure my pet – particularly if the cost of such a policy was not much higher than policies that do require pet health exams and health history. Even more so if they find excuses for not providing you with a written policy in PDF or by mail to look over before the purchase. As Merriam-Webster says, “You get what you pay for, things that can be bought for a very low price probably aren’t very good”.

Then, there is generally a waiting period after you enroll your pet before claims are allowed to be filed. That waiting period can be quite long (~6 months?) for orthopedic (joint and bone) issues. If an orthopedic issue, such as a cruciate ligament tear or elbow dysplasia or vertebral disc issue was diagnosed or signs suggested that issue before you purchased the policy or before the waiting period ended, the claim might be denied. When an orthopedic issue occurred in one leg or the spine before you purchased your policy and then occurs in the opposite leg or another location in the spine, it is often considered the same as a pre-existing, non-covered issue. The same goes for pets that have eaten inappropriate objects before their initial trial period ended.

If your pet already has lumps or bumps on its skin at the time of enrollment and those turn out to be cancerous or infectious after enrollment, they will probably not be covered.

If your pet had any evidence of kidney problems – such as abnormal thirst, increased urination, straining, abnormal urine tests, etc. prior to enrollment, that can be grounds for denying coverage for later problems such as kidney failure. The same goes for prior vomiting, diarrhea, dehydration, constipation, elevated blood pressure or heart issues such as murmurs or abnormal EKGs, x-rays or ultrasound reports. An extended period (often up to 12 months) is often required before skin issues are covered if your pet had any skin issues prior to enrollment or during the waiting period that commenced with enrollment.

If you are a believer in alternative medicine, be sure to ask if the ones you believe in will be covered. Natural supplements, vitamins and foods – whether prescribed or not – are rarely covered. An exception might be made for Hill’s y/d or similar dietary products in lieu of the more expensive radioiodine treatments for hyperthyroidism in cats. Be sure to inquire and discuss that with your veterinarian. In some policies, if your pet contracts any disease against which vaccines are commonly given (such as parvo or distemper or leptospirosis in your dog or panleukopenia in your cat) coverage might be denied.

Google’s Ads and the advertisement departments of other search engines will display just about any ad if it doesn’t contain criminal content and the companies or individuals requesting ad space are willing to pay them to do so. (read here) These ads, also called campaigns or impressions, were said to net Google $54.48 billion dollars in the third quarter of 2022 alone. Ten years ago, Google was already said to be delivering 29.8 billion ads every single day. Today that number would be much larger, defying robotic attempts to police them for accuracy. This page runs Google Ads at the bottom. That is the only way I can keep this website on the air. So, please do not trust what these ads claim to offer you just because you see them on my website. Do your own independent research, deal with companies you already trust for your other insurance needs. I try to block the most spurious (untruthful) ones. But they are like Whac-A-Moles – coming back again and again in new iterations (new versions).

Costs related to breeding, whelping or queening are rarely covered. Be sure to inquire as to your yearly or your pet’s lifetime limits on reimbursements. Also inquire as to how many days notice the company must provide you with if they intend to cancel your pet’s policy (often 60 days).

You are on the Vetspace animal health website

Visiting the products that you see displayed on this website help pay the cost of keeping these articles on the Internet.

{kind=link}

{kind=link}